Keep up with the latest FinTech and private market news, business tips, and thought leadership from industry leaders, mentors, and professionals.

Join our mailing list to receive information on upcoming Helicap platform updates and webinars.

If you're excited about the potential of private markets and fintech, we've got a job for you.

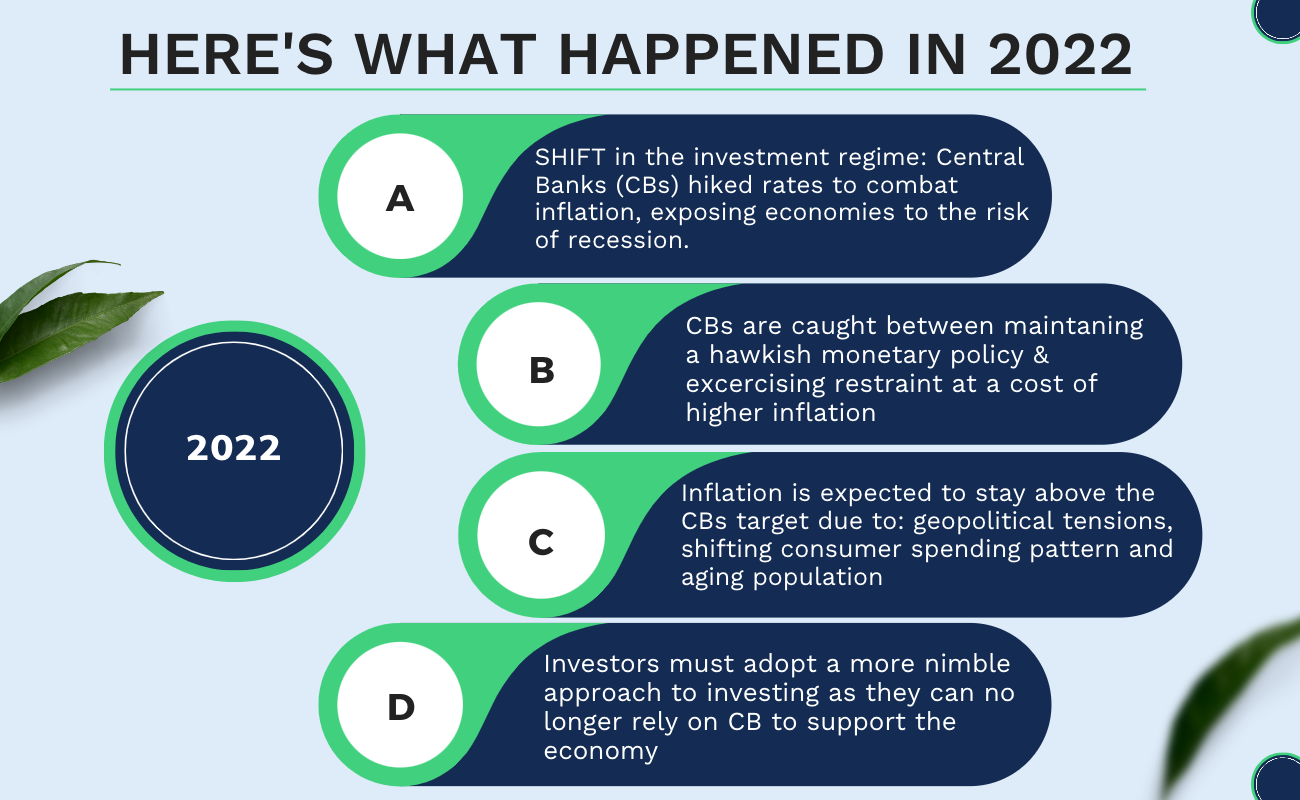

2022 has brought about a paradigm shift. Until last year, the post-GFC era was characterised by rigid central bank focus on economic growth amidst anaemic inflation, a policy which manifested itself in low-interest rates and highly expansionary monetary policy which fuelled one of the most eminent bull runs in recent history. 2022 saw a roundabout turn, as escalating inflation prompted central banks to hike rates with hitherto unprecedented velocity, knowingly and willingly exposing economies to the risk of recession.

Over the past 15 years, investors could rely on the central bank put – whenever the economy started to head south, central banks would step in to support the economy. Under this new regime, investors can no longer count on relief action by the central bank as default backstop, calling for a more selective, more discerning and nimble approach to investing and greater emphasis on real portfolio diversification.

While we believe that the current rate hike and inflation cycle have run the largest part of its course and a cooling in inflation may be on the horizon, we expect inflation to stay well above the 2% level as the central banks declared target. Underlying structural inflation drivers are persistent geopolitical tensions (Ukraine war, US-China rivalry) propelling the cost of energy, food, trade and supply chains, a shift in consumer spending from services to goods and general aging population leading to labour shortages.

This means that central banks will find themselves caught between a rock and a hard place: maintaining a hawkish monetary policy which weighs on demand and therefore economic growth to keep inflation in check, or exercise restraint at the cost of higher inflation. Either way, the leeway for central banks to maintain or even raise their monetary tightening may be limited. The current inflation dynamic is fundamentally driven by supply side constraints, whereas monetary tightening only affects demand, limiting the effectiveness of monetary policy. Perhaps just as importantly, the unprecedented leverage brought about by a decade of quantitative and monetary easing inherently limits the latitude central bankers have in raising rates. Global debt has surged to unprecedented levels as central banks sought to contain the fallout from the pandemic. Consequently, even minor rises in interest rates can have an outsized and painful impact on debt-laden balance sheets. Personal consumers are also not immune to higher rates either, especially those with mortgages. These factors put a lid on the central bank’s scope to hike rates and thus raise the likelihood that higher inflation will become an accepted norm for the foreseeable future.

As a result, policy trade-offs are now much harder. Central banks are likely to veer between favouring growth over inflation, and vice versa. This will result in persistently higher inflation and shorter economic cycles, in our view. The end result: higher risk premia across the board.

Higher interest rates hurt stock prices. The higher the cost of capital deters companies from borrowing and investing to expand their businesses. Earning growth tends to stagnate. There’s also a negative impact on discounted cash flow valuations, which can hurt high-growth stocks. Defensive sectors such as consumer staples and healthcare should prove relatively insulated from lower economic growth expectations, while value stocks tend to perform well in environments of high inflation. From a tactical point of view, the key question is how much of the economic damage is already reflected in equity valuations, which in turn boils down to the interdependencies between inflation, the economy and equity prices, and a view on where we stand in the respective cycles.

It seems that headline inflation has likely peaked for this cycle, with the U.S. Consumer Price Index (CPI) having declined from its reading of 9.1% in June to 6.5% in December, with economic data underpinning this trend: Housing demand and prices are easing, consumer confidence is waning and retail sales growth is showing some signs of stalling. This suggests CPI may have room to come down further, giving the Fed room to put the break on its rate-hiking campaign. While inflation peaks have historically coincided with market bottoms, it is important to note that recession onsets are called in hindsight ― once the National Bureau of Economic Research (NBER) analyses past data and makes a formal declaration. While the common shorthand definition of a recession are two consecutive quarters of negative GDP growth, an official declaration relies on a far more complex assessment involving multiple metrics (such as real personal income, unemployment rates, consumption, retail sales and production), a complexity which tends to contribute to a time lag between occurrence and declaration of a recession. Other evidence suggests equity bottoms most often take place during a recession.

Similarly, the market bottom may only be clear in hindsight, with much of it hinging on the Fed and its read of inflation and the economy. A recession seems not unlikely, for a few reasons. History suggests that inflation above 5% is a recipe for recession. And this time around, the Fed has made dramatic rate moves in a short time to catch up from a late start in addressing inflation. Empirically, the impact of the Fed’s actions on the real economy tends to unfold with considerable and variable lags, so the economic consequences are yet to fully materialize. Against this backdrop, stocks are likely to remain subject to considerable uncertainty and volatility, and we believe a focus on resilience remains paramount in equity portfolios. This includes stocks with quality characteristics and positions that seek to balance offsetting risks (e.g., value coupled with growth; defensives alongside cyclicals).

As central banks ratchet up interest rates to contain inflation, high-grade bonds are starting to give stocks a run for their money. As bond yields reset at higher levels, inflation peaks, and central banks stop rate hikes, hard currency bonds and selected yield curve steepening strategies may look attractive in principle. However, record high debt levels, quantitative tightening and higher risk premia call for cautionary and discriminatory approach to investing in the public markets. In addition, higher inflation has raised the threshold for real return generation and indeed, real returns of 10yr USTs (i.e. nominal yield adjusted for inflation measured by CPI) have actually fallen between Dec ’20 and Dec’22, from -0.5% around to -2%

All being said, the days of the generalised bull market which we experienced over the past decade seems numbered. Volatility is here to stay with headlines over global shocks becoming increasingly regular. The ability to generate alpha through careful, selective and tactical selection of stocks and bonds will be ever more important in a macro-environment characterized by geopolitical uncertainty and elevated inflation where investors can no longer count on the central bank to prop up the stock and bond markets.

Private credit has expanded as banks have withdrawn from lending, largely as a result of regulatory changes. While the past year’s turmoil has shaken markets, companies continue to require financing – and they are increasingly turning to private lenders. While higher interest rates and credit risk premia the risk of higher default rates, this can be mitigated through disciplined investment selection and deal structuring, which is easier in private arrangements and can provide opportunities for rescue financing.

Even in a rising interest-rate environment, the illiquidity premium offered by private credit is an important way to generate additional yield, at comparable or even lesser risk exposure risk. The premiums offered by private credit vary depending on names, structure and macroeconomic conditions. But on a like-for-like basis, private senior and unitranche loans tend to offer a premium estimated to be 150bps and 300bps relative to, publicly traded (leveraged) loans.

The raise in interest rates has caused turmoil in the financial markets. But it could be a boon in private credit because of bespoke nature implies the flexibility to react to changing market conditions and adjust financing terms accordingly. In opportunistic credit, investors are increasingly able to benefit from innovative coupon structures combining on floating rate coupons with a minimum guaranteed IRR floor, or to extract greater equity participation from corporates who prefer credit to raising dilutive down rounds of equity capital.

That said, we believe that in the current environment of elevated rates and refinancing costs, the importance of rigorous underwriting standards and clever deal structuring is greater than never before in order to generate credit alpha. This includes robustly structured deal terms safeguarding the seniority in the payment waterfall and recourse to security collateral, as well as stringent covenants permitting early intervention and restructuring in case of a deterioration in the obligors financial or operating performance. Unlike for public debt or bank syndications, the direct lending nature of private debt generally allows skilled private debt originators to negotiate and incorporate relevant security and covenant packages into the transactions for the benefit of investor lenders. As such, it is not surprising that private debt has over time not only had lower default rates than high yield bonds (during the global financial crisis, default rates on junk bonds spiked out to 12 percent, whereas private debt defaults peaked at just half that), but also higher recovery rates. With the added benefit of higher rates, wider credit spreads and customised security packages, the risk-return profile of private credit as an asset class may well be more attractive than it has ever been, while at the same injecting true diversification and resilience into investment portfolios.

Investment involves risk. Past performance is not necessarily a guide to future performance or returns. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested. Rates of exchange may cause the value of investments to go up or down.

Any forward-looking statements, prediction, projection or forecast on the economy, stock market, bond market or economic trends of the markets contained in this material are subject to market influences and contingent upon matters outside the control of Helicap Pte. Ltd. (“Helicap”) and therefore may not be realised in the future. Further, any opinion or estimate is made on a general basis and subject to change without notice. In presenting the information above, none of Helicap, its affiliates, directors, employees, representatives or agents have given any consideration to, nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Therefore, no representation is made as to the completeness and adequacy of the information to make an informed decision. You should carefully consider (i) whether any investment views and products/ services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances. You may also wish to seek financial advice through a financial advisor or and independent legal, accounting, regulatory or tax advice, as appropriate.